The economic, or fair value, of rollover equity is often unknown at the time of a transaction and frequently either not specified in a purchase agreement, or erroneously stipulated based on oversimplified estimates. Commonly, the value ascribed to rollover equity in purchase agreements does not consider all of the rights, preferences, and limitations that may apply to and significantly impact the fair value of the rollover equity. This can be a significant financial reporting hurdle for properly accounting for business combinations pursuant to ASC 805 as the fair value ascribed to the rollover equity can impact the calculation of consideration transferred, goodwill, and the fair value of intangible assets. The good news is that the valuation and accounting professions have developed widely accepted procedures for accurately estimating the fair value of the rollover equity in a transaction.

BACKGROUND

Financial buyers frequently structure deals with various levels of cash, debt, contingent considerations, and often a form of consideration known as rollover equity. Rollover equity is designed to incentivize high performing management teams to remain with the company after the transaction has closed by allowing management to continue to benefit from the increase in the value of the company over time based on continued ownership of some amount of equity. However, the form of equity assigned to rollover holders can be structured in ways where participation in future value creation does not necessarily lend itself to intuitive present value indications. As a result, an overly simplistic estimation of the value of rollover equity may vary significantly from the fair value and, in turn, the fair value of opening balance sheet items could be significantly impacted.

CONSIDERATIONS

For estimation of the rollover equity value pursuant to ASC 805, it is critical to understand the various factors that may cause simplified value estimates of rollover equity to differ from the fair value of the rollover equity which complies with financial reporting standards. These factors can include, but are not limited to:

- Subordination features – rollover equity may take a lower priority position in liquidation scenarios than that of the preferred equity held by the private equity sponsor. This generally puts downward pressure on the value of the rollover securities, all else equal.

- Return preferences – in some cases, the financial sponsor’s equity and the rollover equity may have differing return preferences. A careful analysis of these differences should be performed to determine the impact on the fair value of the rollover equity.

- Conversion features – if the purchased equity is a preferred share, but has rights to convert to common, the potential dilution should be taken into consideration as a difference in the value of the shares owned by the private equity sponsor and that of the rollover participants;

- Promote structures – distribution waterfalls can have various promote structures at different levels of value creation which accrue to equity holders at different rates. Therefore, understanding how the distribution waterfall works can impact the estimation of fair value of the rollover equity retained by management.

- Marketability1– in many cases minority interests in privately held companies do not have the unilateral ability to sell the Company and convert their shares into cash. Therefore, this lack of marketability can reduce the fair value of the rollover equity.

Due to the complexity of deal structures a valuation specialist can be a tremendous asset in evaluating the economics of a transaction including the fair value of the rollover equity.

EXAMPLE:

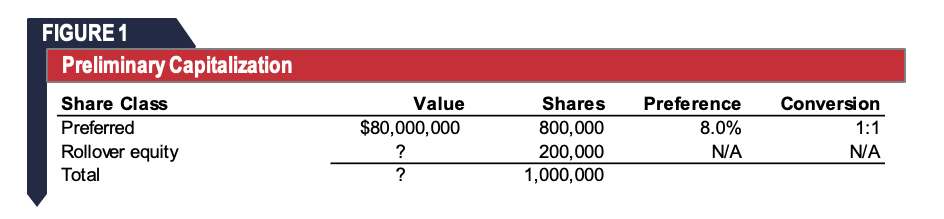

Let’s say that for $100 per share the buyer purchases 800,000 shares of preferred equity which carry an 8 percent preferred return and are convertible to common shares at a 1:1 ratio, and that the seller receives 200,000 common equity shares. Based on the description of the preferred securities purchased by the private equity firm, it would be inappropriate for financial reporting purposes to assign a $100 per share value, or $20 million to the rollover units. The question is how much different could the fair value be?

To value the rollover equity in this type of scenario, valuation practitioners often employ the back-solve method. This method uses the known transaction value of one share class to determine the implied value, or the “backed into value,” of another share class by using an allocation method which bifurcates the value of the company’s total equity to its various share classes such that the value distributed to the known share class is equal to the price paid for it. The standard allocation methods used in the valuation industry are called the option pricing method (“OPM”), the probability weighted expected returns method (“PWERM”), and the hybrid method. These methods may be driven by various techniques such as Monte Carlo simulations or the Black-Scholes option pricing model. While an option method may not be intuitive to some because the rollover equity is not on its face what some consider a traditional derivative security, the economic payout of the equity interests can be modeled in a way that is consistent with option pricing theory. That said, each of the valuation methodologies has advantages under different scenarios and should be carefully considered in selecting a particular model.

In this case, we assume the following: the private equity sponsor paid $80 million for the preferred shares, the timing of exit is known, the expected future values of the company’s total equity are lognormally distributed, and market based inputs for the Black-Scholes model such as risk free rates and volatility are reasonably attainable. Therefore, we can utilize the OPM with the Black-Scholes model such that the allocated value of the preferred shares equals the known purchase price.

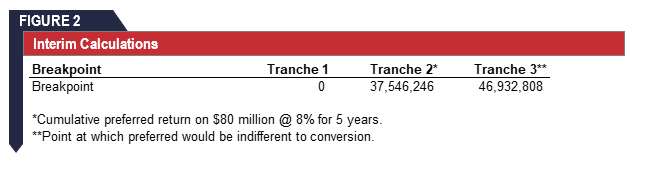

The first step is to calculate break points at which to allocate values in accordance with participation of the capital holders. The first break point, at the end of tranche 1 (and beginning of tranche 2), is the point that equals the preferred capital plus the stated preferred return. The second break point is the point at which the preferred shareholders are indifferent to converting or not converting into common equity. In the example below we have assumed that there will be a liquidation event in 5 years (a common holding period for private equity companies). Before the first breakpoint, the preferred equity holders would have rights to 100 percent of the distributable cash flows equal to the cumulative preferred return since the preferred class is senior to the common share class. However, after the total equity distributions reach an amount greater than the cumulative preferred return of $37.5 million, the rollover equity would receive 100 percent of the proceeds up to the point at which the preferred holders would be economically incentivized to convert to common shares and receive 80 percent of distributions above the second breakpoint and the rollover shareholders would receive 20 percent of the remaining distributions.

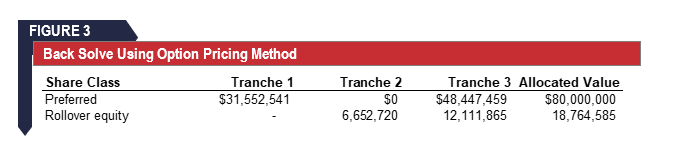

We can think of the rollover equity having a value equal to a call option on the company’s total equity with an exercise price equal to the cumulative preferred return, adjusted for its participation in the total expected upside potential over such an amount. Therefore, we can use the Black-Scholes option pricing formula to estimate the values of each tranche of participation. Inputs to the Black-Scholes model include the time to liquidation, the risk-free rate with a maturity corresponding to the time to liquidation, the volatility of future equity prices often estimated based on the volatility of a group of publicly traded peers, the cash dividend yield of the company, and an exercise price which corresponds to the tranche breakpoints. Below is an example of the output of an OPM using a Black-Scholes model after calibrating the known value of the preferred stock to the purchased price and allocating the remaining value to the rollover equity.

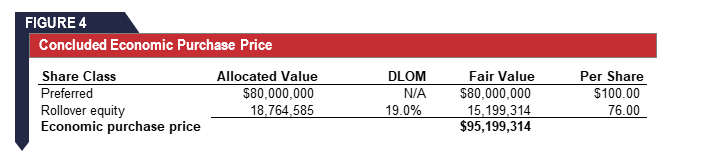

Lastly, because rollover equity is typically a minority equity interest of a closely held company, it is appropriate to apply an adjustment to the allocated value calculated above to reflect the lack of marketability of the rollover interest compared to marketable securities from which the other valuation inputs were derived. One method of quantifying a discount for lack of marketability uses an Asian Put option pricing model which includes inputs similar to those previously used in the Black-Scholes model for allocating value in the OPM. However, because leverage within the total equity class impacts the variance of the prices of each class, it is appropriate to calculate class specific volatility as an input. Class volatility can be estimated based on guidance provided in the AICPA Accounting & Valuation Guide: Valuation of Privately-Held-Company Equity Securities Issued as Compensation, Section 7.32. The AICPA recommends the use of a differential discount for lack of marketability (“DLOM”) model, which in the case above results in a 19 percent downward adjustment to the previously allocated value of rollover equity.

The indication of fair value of the rollover equity in this example is significantly discounted from a simplified approach in which the differences between the share classes are ignored. Because deal structures and covenants for different share classes can vary widely, the difference in a simplified allocation estimate and one that complies with fair value accounting standards could be greater or less than the amount estimated in this example. In any case, however, auditors will expect the fair value of the rollover equity to comply with accepted accounting standards as the calculation of the consideration transferred is the starting point for determining the fair value of other assets and liabilities pursuant to ASC 805.

WRAPPING UP

While deal structures that include rollover equity can incentivize management to maintain high performance, they can also create challenges for accurate fair value measurements of certain assets, liabilities, and considerations used in financial reporting. Professionals experienced with calculating the fair value of rollover equity may be extremely helpful in providing fair value estimates which comply with standards outlined in ASC 805 and valuation guidance offered by the AICPA. The BVA team has extensive experience in valuing rollover equity in the context of ASC 805 fair value standards. Contact one of our experts if you would like to discuss the details of your transaction or fair value accounting needs.

1While it is appropriate to consider potential marketability discounts, it is typically not appropriate to apply discounts for lack of control. While the rollover equity interest is typically a minority interest, it is best practice to utilize market participant cash flows in most situations involving rollover equity which assumes that the lead investor would optimize cash flows of the business, rendering little or no difference in the cash flows anticipated by control level and minority level investors. Accordingly, in many situations, it is not necessary to apply a discount for lack of control to the rollover interest. However, we acknowledge that even when investor cash flows are expected to be optimized, a minority interest in a closely held company would be more difficult to sell, thus a discount for lack of marketability is often warranted.