The US Congress today finalized the major provisions of the CARES Act stimulus package, which will likely be signed by President Trump by the end of the weekend. The stimulus package includes numerous provisions to support business payrolls, unemployment benefits, and cash payments to lower-income Americans. The policies included within the package mirror traditional measures used to alleviate recessions; however, the measures may fall short of preventing an oncoming consumer debt default wave.

As we learned from the most recent financial crisis and great recession, the long-term benefit of income support programs and traditional monetary policy measures on default rates are limited. Within a year of the financial crisis, mortgage delinquency rates approached 10%—even with emergency unemployment benefits and stimulus measures.

Measures taken by the banking industry had similarly limited benefits. Modification policy posed many well-documented problems. Cumbersome paperwork and documentation requirements for borrowers confused and delayed social benefits, the taxability of principal reduction modifications disincentivized the use of loan modifications for cash-strapped borrowers, and prohibitions or limitations on modifications imposed by private-label conduits reduced the comprehensiveness of relief—particularly to those borrowers who needed it most. Servicing operations were stressed not only with volume but also with new costly and unwieldy regulations.

With this, it is no surprise then that banking industry commentators continue to predict a tsunami of defaults and new delinquencies headed for servicers and investors from the current economic crisis. Indeed, a number of factors indicate even greater potential difficulties related to consumer debt in response to the COVID-19 pandemic.

Servicers face extensive capacity constraints in their ability to implement relief plans and programs. The Financial Times reported that mortgage lenders in the UK are already reporting that call centers are "inundated with anxious homeowners seeking mortgage holidays." Kate Berry, in a March 24th American Banker article, wrote that a similar situation is likely to unfold soon within the US, quoting Ted Tozer, a senior fellow at the Milken Institute and the former president of Ginnie Mae, commenting that granting two to three million payment deferrals on a one-by-one basis is going to "overwhelm the system.”

Not only will the magnitude of such calls overwhelm an otherwise healthy system but the servicers, themselves, are at the same time dealing with staff cutbacks resulting from social distancing requirements. Again, according to Berry, Scott Buchanan, executive director of the Student Loan Servicing Alliance, said that several servicers have had to stagger their shifts in order to re-seat call-center workers, which has limited the firms’ capacity to take calls from customers. He noted that servicers have emergency preparedness plans but added, “I think this is a scale that probably very few companies have contemplated.”

A three-month shock to mortgage debt alone could yield upwards of $1.25 billion - $1.86 billion in incremental servicing costs based on MBA’s speculated 25% default spike (impacting two to three million loans) and the FDIC’s estimated $2,500 per year servicing cost for delinquent loans. For servicers with already tight liquidity levels, these potential increased costs (in addition to the cost of funding their advance obligations) are substantial.

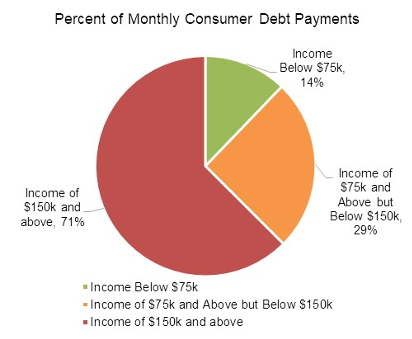

Income support may be too little, too late. US consumer debt-to-income ratios tend to rise as income approaches $250k, meaning household borrowers just above the cash-payment phaseout level of $75k per individual/$150k per couple are the most leveraged. Indeed, 2016 SCF data shows that nearly 70% of monthly consumer debt payments are made by households with incomes above $150k annually. Concentration of consumer leverage of American households earning above $150k is a key reason the prior financial crisis was heavily driven by Alt-A mortgages, rather than the more widely discussed subprime mortgages.

Source: Survey of Consumer Finance Summary Extract Public Data using the SDA Analysis tool.

In monthly terms, the $1,200 one-time stimulus payment amounts to less than one monthly debt service payment for households with incomes over $150k and less than two payments for those making $75k annually. Similarly, the expanded unemployment benefit of $600 per week (or ~$2,400/month) will only fill a portion of the debt service for unemployed for households making over $75k, as their income will decrease substantially even with those additional benefits.

Together, the income support programs, while helpful to mitigate effects and keep households afloat, are a drop in the bucket in comparison to normal living expenses, rent and mortgage payments, and other consumer debt payments.

So far, the policy response has been toward alleviating a recession arising from a financial crisis instead of reducing the uncertainty accompanying a natural disaster. Natural disaster mitigation strategies focus on immediate aid, parachuting supplies, equipment, and support to those in need in order to introduce an element of control to the situation.

To date, however, the US policy responses (ranging from testing policy to economic aid) to the COVID-19 pandemic have done little to quell consumer, investor, or general market fears. As such, economic uncertainty continues to evolve at a rapid pace on a day-to-day basis, putting greater strain on businesses facing upcoming financial reporting deadlines and consumers facing the gauntlet of looming debt payments.

Monetary economists know that uncertainty adds to business cycle depth and duration. At this stage of the crisis, the tradeoff facing creditors and investors in consumer debt is to take a known hit by instituting a three-month payment holiday today and locking in the quantifiable, predictable liquidity and valuation effects or turn their backs to the coming wave and face the uncertain effects as consumers default in greater magnitude and for longer periods than they would otherwise.