The COVID-19 pandemic impacted just about every sector of global commerce. The insurance sector, while less directly affected than some industries, was nevertheless significantly impacted. Over the course of 2020, the S&P Insurance Industry Index (ticker INDEXSP:SPSIINS) lagged behind the overall S&P 500 market index by 20.8 percent. The insurance industry declined more sharply than the market as a whole in the initial wake of the COVID-19 pandemic. However, the insurance industry did not participate as fully in the rally in the latter half of the year, as demonstrated below:

.png)

Data Provided by CapitalIQ

The focus of this article revolves around the key drivers in each of the subcategories in the insurance industry and how the COVID-19 pandemic impacted these areas of the economy in 2020.

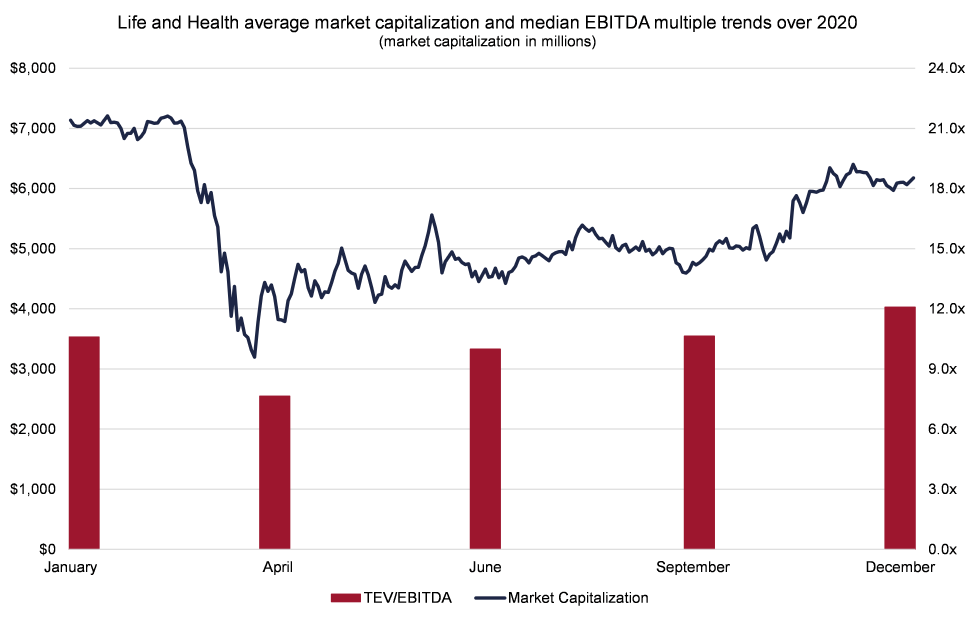

LIFE AND HEALTH INSURANCE

The penetration rate of life insurance over the last decade has declined significantly in the United States, with the penetration rate of the life insurance industry falling to 2.9 percent in 2019 as compared to 3.9 percent in 2008. Additionally, low interest rates, which have been prevalent since the Great Recession, have hampered portfolio returns. Finally, an aging insurance workforce highlighted difficulties that this sector would have in navigating the new digital decade.1

In 2020, the sector saw a meaningful decline in demand for its services as a result of increased uncertainty in the financial stability of individuals, rising unemployment, and lower investment income.2 Accordingly, the average market capitalization of publicly traded life and health insurance companies in the United States decreased by 13.4 percent, as shown in the below illustration. Enterprise value to earnings before interest, taxes, depreciation, and amortization (EBITDA) multiples dipped in the first quarter of 2020 as the market reacted to the economic fallout of the COVID-19 pandemic and recovered throughout the remainder of the year.

Globally, key growth drivers seen in the industry included premiums written in developing economies, which accounted for 52.0 percent of growth through 2019. However, 84.0 percent of the growth in individual annuity market came from developing markets:3

Data includes insurance companies under the Life and Health segment, provided and defined by CapitalIQ

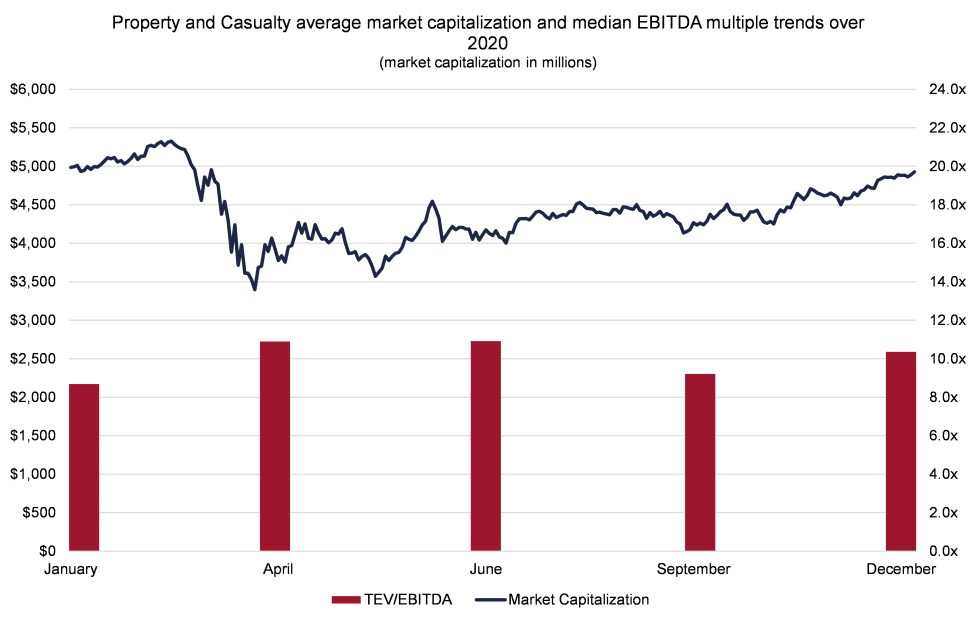

PROPERTY AND CASUALTY INSURANCE

North America comprises 40.0 percent of the global property and casualty (P&C) market and was hit notably hard by pandemic and catastrophe-related losses.4 In the first half of 2020 alone, P&C insurers saw annualized operating return-on-equity fall from 8.3 percent to 2.8 percent. This loss is evidenced by $6.8 billion of incurred losses related to the COVID-19 pandemic, including workforce reductions resulting in workers compensation insurance sales falling (with the recovery of this segment expected to be slow until employment rebounds to prepandemic levels). Additionally, as many small businesses closed in 2020 due to pandemic-related shutdowns, premiums sold to these businesses may also be slow to recover.5

While 2020 was a challenging year for the P&C industry overall, results were more mixed for the automobile insurance segment. While the auto segment also saw reductions in premiums due to changes in driving habits and decreased demand for policies, insurers experienced an uptick in profitability due to a drop in accident frequency.6 Accordingly, the average market cap of P&C firms in the United States stagnated during 2020 with a large decrease in the first half of the year, followed by a prolonged recovery. Average enterprise value to EBITDA multiples initially rose in the first quarter of 2020 as the sharp decline in trailing EBITDA outpaced the decline in enterprise value. However, enterprise value to EBITDA multiples stabilized thereafter to remain largely unchanged over the course of the year.

Data includes insurance companies under the P&C segment, provided and defined by CapitalIQ

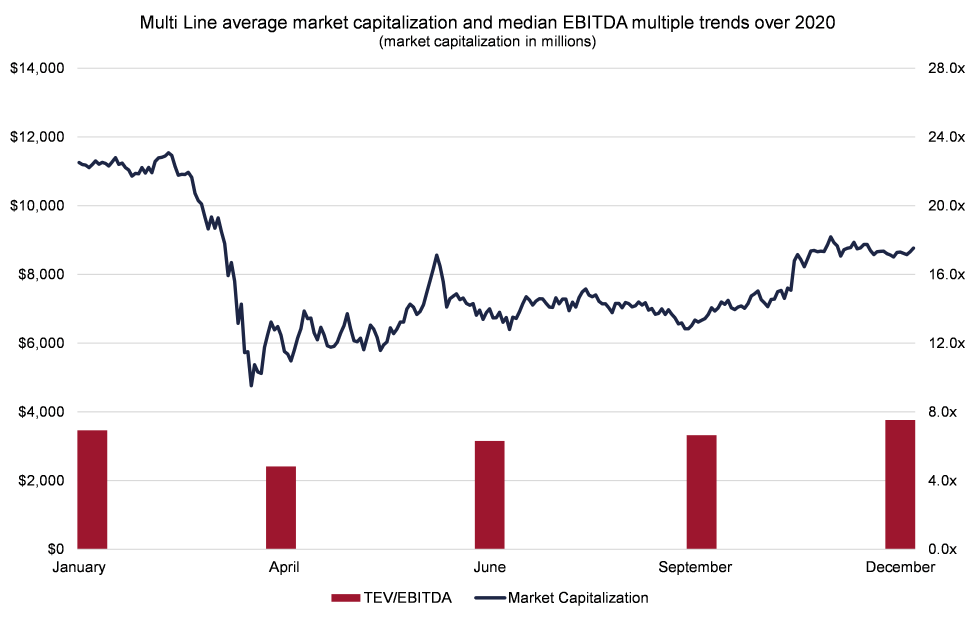

MULTILINE INSURANCE

Due to the correlation with the life and health and P&C markets, multiline insurers were faced with significant challenges due to COVID-19 and their exposure to risks seen across the insurance spectrum by their customers. International multiline insurers, Allianz and AXA, and US giant, Hartford, all noted revenue and profit declines as compared to 2019 results.7 The Hartford's 2021 guidance for its commercial combined ratio indicates management expects better profits in this sector. (Combined ratio represents the sum of the calendar year loss ratio and the trade basis expense ratio.) However, this may be burdened by an increase in the combined ratio for personal lines of insurance.8

With respect to publicly traded constituents of this subindustry, US-based multiline insurers saw the largest decreases to average market capitalization out of the 5 component industries, decreasing 22.1 percent over the year. Similarly, earnings sharply declined in 2020, as shown below. Multiples of enterprise value to EBITDA initially declined in the first quarter of 2020 with the economic impact of the COVID-19 pandemic but recovered in the remaining three quarters.

Data includes insurance companies under the Multi Line segment, provided and defined by CapitalIQ

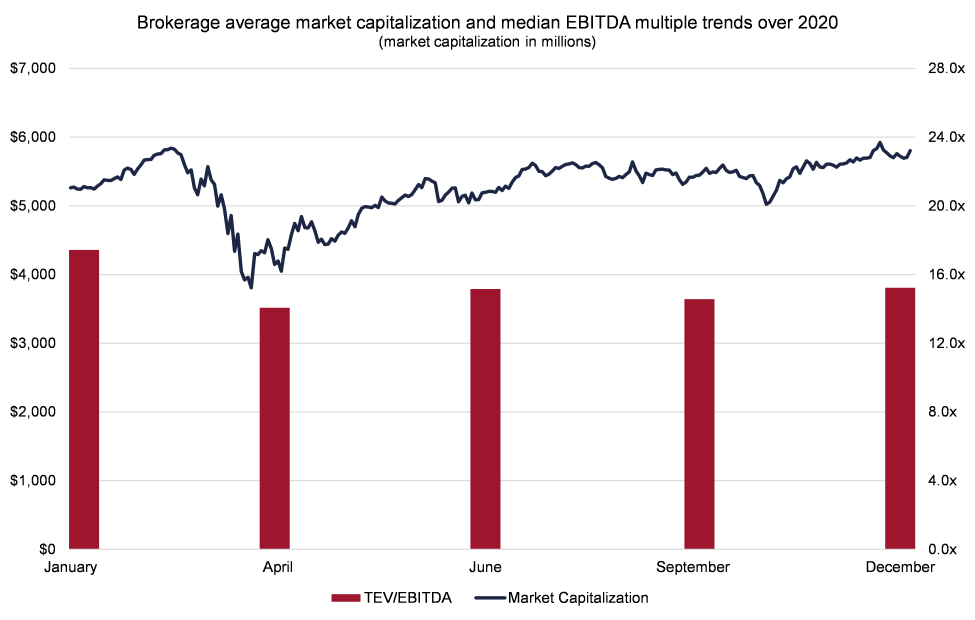

INSURANCE BROKERS

Marsh and McLennan, one of the largest brokerage firms in the world, reported growth of 9.0 percent on adjusted operating income, while AON plc reported operating income growth of 4.0 percent,9 with positive indicators such as the change in the homeownership rate increasing from 2019 to 2020 by 0.8 percent and peaking in Q2 of 2020 at 67.9 percent.10 Brokerage firms were able to navigate the pandemic nimbly and benefitted from a lack of risk exposure. Brokerage firms increased their average equity market capitalization by 10.1 percent over 2020, as compared to an aggregate decrease in average market capitalization across the broader insurance sector of 7.2 percent.

An additional positive note for brokerage firms is that they were the only portion of the insurance industry to record an increase to average EBITDA over 2020. Because market capitalization appreciated at a similar rate, multiples of enterprise value to EBITDA were fairly stable over the course of the year, as demonstrated below, except for an initial decline in the first quarter of 2020 in the wake of the economic impact of the COVID-19 pandemic.

Data includes insurance companies under the Brokerage segment, provided and defined by CapitalIQ

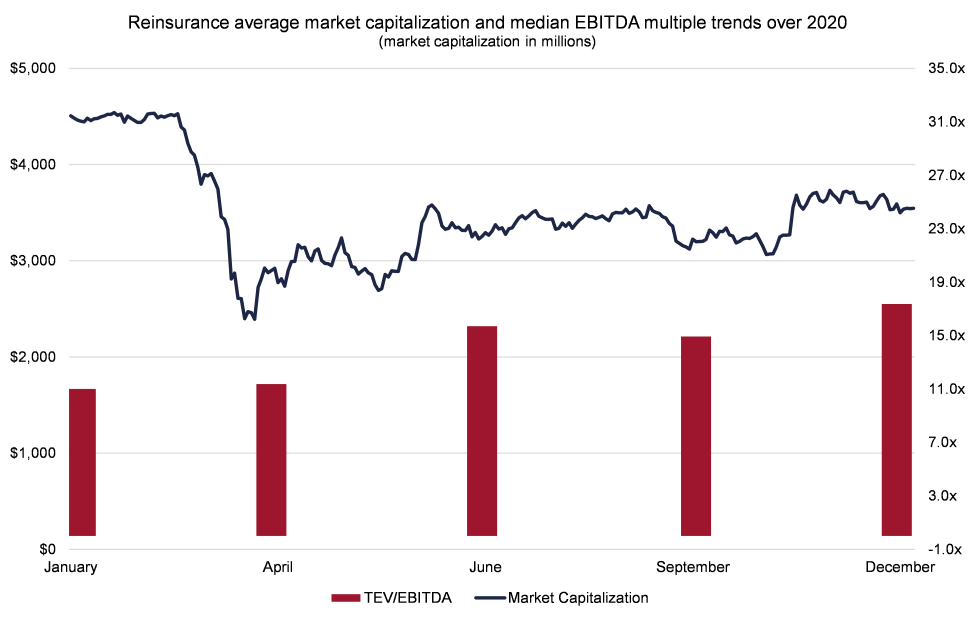

REINSURANCE

Reinsurers exercised caution in 2020. Given the complexity in navigating the COVID-19 pandemic, reinsurers deployed strict transaction guidelines in order to make smart decisions, which resulted in the lowest percentage of excess reinsurance authorizations for catastrophe insurance since 2012. Dedicated capital, as estimated by Guy Carpenter and A. M. Best, was down slightly over 2.0 percent through midyear 2020. Along with this, due to increasingly complex risk environments dating back to prepandemic, the reinsurance market is expected to continue with lengthy and complex negotiations into 2021.11

Valuations of international reinsurers suffered the greatest out of the global insurance industry, decreasing in market capitalization by 21.3 percent over 2020. Similarly, the average earnings for global reinsurers declined dramatically. As a result, despite the decline in market capitalization, average enterprise value to EBITDA multiples expanded from 11.0x in January to 17.4x in December.

Data includes insurance companies under the reinsurance segment, provided and defined by CapitalIQ.

All public companies were evaluated due to limited data on US-based reinsurers.

TRANSACTIONS

Mayer Brown, LLP, notes that, while transactions were "virtually halt[ed]" through the first half of 2020, second-half activity was more than enough to make up for the languid markets in the first half of the year, with overall activity finishing above the 2019 level.12 Some notable transactions during 2020 included Allstate's purchase of National General Holdings in an all-cash deal for about $4.0 billion, increasing Allstate's market share in personal property-liability.13 Additionally, Allstate chose to divest of its life insurance group, selling the group for $2.8 billion to Blackstone in order to focus on the aforementioned personal property-liability market.14

InsurTech was a hot area for transactions in 2020 as well, with a Softbank-backed firm going public at a valuation of over $1 billion and Metromile completing an $842 million reverse merger with a special purpose acquisition corporation.15 Private equity investment in the space was capped by KKR's majority stake investment in Global Atlantic Financial Group, purchased at book value of equity of approximately $4.4 billion.16

CONCLUSION

Overall, the insurance industry, both domestically in the United States and globally, was negatively impacted by the COVID-19 pandemic. Market capitalizations decreased, although most segments of the insurance market rebounded in the latter half of 2020, but in most cases, to a lesser degree than the markets as a whole.

Although most segments of the insurance industry rebounded in the latter half of 2020, market capitalizations were still down on the year and saw less recovery than the market as a whole, with EBITDA declining throughout the year. As a result, in many segments, enterprise value to EBITDA multiples increased throughout the course of 2020. Looking forward, industry revenue is expected to increase over the next 5 years as premium prices are expected to rise. Similarly, interest rates are expected to rise, increasing expected portfolio returns.17

12020 US and Americas Insurance Outlook, Ernst and Young, December 5, 2019.

2The Future of Life Insurance: Reimagining the Industry for the Decade Ahead, McKinsey and Company, September 29, 2020.

3McKinsey and Company.

4Matthew Lerner, "Property/Casualty Insurance Sector Outlook Stable for 2020: Moody's," Business Insurance, December 5, 2019.

5Gary Shaw and Neal Baumann, "2021 Insurance Outlook," Deloitte, December 3, 2020.

6Shaw and Baumann.

7"Full Year 2020 Earnings," AXA, February 25, 2021; "Highlights Fiscal Year 2020," Allianz, 2021; "The Hartford Announces Fourth Quarter and Full Year 2020 Financial Results, 2021 Outlook for Select Business Metrics," The Hartford, February 4, 2021.

8The Hartford.

9"Investor Presentation: Results through Fourth Quarter 2020," MarshMcLennan Companies, 2021; "Aon Reports Fourth Quarter and Full Year 2020 Results," Aon plc, February 5, 2021.

10"Homeownership Rate for the United States (RHORUSQ156N)," FRED Economic Data, February 2, 2021.

11"Leading Up to January 2021 Reinsurance Renewals," Guy Carp, March 2021.

12"2020 Global Insurance Summary and Trends for the Future," Mayer Brown, March 2021.

13Allstate Form 8-K, dated July 8, 2020.

14"Allstate Announces Agreement To Sell Allstate Life Insurance Company," Business Wire, January 26, 2021.

15Luisa Beltran, "Insurance Is Hot Again: Allstate, KKR Launch M&A Deals after Lemonade IPO," Barron's, July 8, 2020.

16"KKR To Acquire Global Atlantic Financial Group Limited in a Strategic Transaction," Global Atlantic, July 8, 2020.

17"Finance and Insurance in the US—Good investment: Interest Rates and Access to Credit Are Expected To Rise, Supporting Sector Growth," IBISWorld, November 2020.